Weekly review: Good news frequently helped the dollar to re-start the oil price and climb the new high. Gold is still at risk.

In the past week, the US economic data was optimistic. The Trump tax reform plan further reduced the obstacles. The European Central Bank’s interest rate decision was biased towards the doves. The US dollar index rose about 1% to a three-month high, recording the largest single in the past six months. Weekly gains are expected to regain the mid-line gains; while gold and silver and most non-US currencies are significantly dragged down, spot gold falls below the 100-day moving average, and the euro also fell nearly 1.5%; affected by OPEC’s call to extend the production cut, oil prices also hit New high in the past six months.

★List of important economic data and important risk events this week

First, the optimistic US economic data, the Fed’s interest rate hike in December has been “suggestedâ€

This week, the United States released a series of economic data, the overall performance is more optimistic, to provide further support for the Fed to raise interest rates at the end of the year, but also provides the dollar index with a rising momentum.

First, market research firm Markit announced the US October Markit manufacturing PMI and other relevant data. The initial performance of the US service industry and manufacturing industry exceeded expectations in October, rising to a nine-month high, pushing the comprehensive PMI index to rise to January. The highest point.

(America's Markit manufacturing PMI and other data performance at a glance)

Second, US new home sales soared to nearly 10 years in September, and signs of accelerated property market growth have raised expectations that the Fed will raise interest rates again in December. According to the specific data, US new home sales in September surged 18.9% from August, with an annual rate of 667,000. The first month of September US durable goods orders announced on the same day increased by 2.2%, which is better than the market expectation of 1% growth, suggesting a strong growth in US equipment investment in the third quarter.

Third, the market's most concerned US third-quarter GDP grew by 3% quarter-on-quarter, which is better than the market expectation of 2.6%.

According to Huitong.com, the US federal funds rate futures show that the Fed’s probability of raising interest rates in December has reached 85.3%, while the probability is only 20% at the beginning of September; it is only about 67% at the beginning of October; After the interest rate decision, because of the US dollar press conference arrangement, there will be no interest rate hike in November; according to historical circumstances, if there is no particularly serious accident, the Fed’s interest rate hike in December is basically a matter of fact.

(US federal funds futures interest rate futures)

Second, the European Central Bank's interest rate decision is a bite, the euro was sold off or started the mid-line decline

One of the biggest risk events of the week is naturally the interest rate decision announced by the European Central Bank on Thursday (October 26). The European Central Bank maintains the current interest rate as scheduled and extends the bond purchase plan by nine months until the end of September 2018. From January 2018, the monthly bond purchases were reduced to 30 billion, including the day's press release. European Central Bank President Mario Draghi's speech was generally biased towards doves, which caused the euro to sell off against the US dollar, which fell 160 points that day. , a drop of more than 1%, the worst single-day performance in 16 months.

European Central Bank President Mario Draghi said on Thursday that the European Central Bank will reduce the monthly bond purchases to 30 billion euros in January. The purchase of bonds will last at least until September 2018, and if necessary, it will expand the scale of debt purchases or extend Time; the bond purchase plan is flexible enough to deal with limitations; reducing the size of monthly bond purchases is not equal to minus.

Draghi also said that interest rates will remain at current levels and continue for a long time after the end of QE. The QE parameters and restrictions were not discussed in this meeting. The ECB did not discuss the substitution of QE; the majority of the members supported the QE open ending, and the support did not set a specific deadline for QE, and QE would not end in summer.

Carsten Brzeski, an economist at ING in Frankfurt, believes that the ECB's decision is a huge change, but it is also very modest and does not mean a major turning point in the ECB's monetary policy.

The economist also pointed out that, in fact, the recalibration of the quantitative easing program announced by the European Central Bank indicates that the bank wants to exit the easing policy as cautiously as possible, ideally not to cause the euro to appreciate or the bond yield to rise. . This is a very “doves†practice of reducing monetary stimulus.

Omer Esiner, chief market strategist at Commonwealth Foreign Exchange, also believes that the European Central Bank is open to further extensions to the bond purchase program, a dovish tone that has surprised the market.

After the European Central Bank announced the interest rate decision, the euro continued to decline against the US dollar. On Friday (October 28), it once refreshed the three-month low to 1.1575. Of course, this is also the optimistic performance of the US economic data. The US tax reform plan is expected to improve. .

In view of the fact that the euro fell below the important support of 1.1660 and 1.1615 this week, the further downside risk of the mid-line has increased significantly. Currently, it is barely supported by the mid-rail of the weekly Bollinger Band 1.1564. Once it falls below, it is considered that the technical side of the weekly line is good. After the operation, the euro against the US dollar or gradually oscillated at least to fall to the 1.0340-1.2091 rally in the 38.2% retracement near 1.1422.

(EUR/USD weekly chart)

Third, the US tax reform plan will remove another obstacle, and the dollar’s ​​“head and shoulders†will form a bullish pattern.

Another event that has had a major impact on the financial market this week is the tax reform plan for the United States. The US House of Representatives Republicans passed a 2018 fiscal year budget on Thursday (October 26), which opened a rush for US President Donald Trump to achieve large-scale tax cuts before the end of the year. The channel, which also helped the dollar index, which has been oscillating since 2017, initially established a technical pattern to regain the mid-line rally.

According to Huitong.com, the House of Representatives passed the budget resolution on Thursday with a vote of 216-212, paving the way for the Republican Party to promote tax cuts without the support of the Democratic Party. The resolution will allow the US fiscal deficit to increase in the next decade. $1.5 trillion to support the Trump administration's massive tax cuts while allowing the Senate to pass the tax reform bill with a simple majority of 51 votes. Without the above terms, the Senate needs 60 votes to pass the tax reform bill.

It is worth mentioning that the Senate approved the 2018 fiscal year budget with a vote of 51 to 49 on Thursday (October 19).

Market analysts pointed out that the tax reform will greatly reduce the tax burden of US residents, especially the tax burden of the middle and low income groups in the United States. In this tax reduction plan, the overall average tax revenue decreased by 21%. Since the proportion of US personal consumption expenditure to disposable income is relatively stable, it can be estimated that tax reform will release about 300 billion US dollars in personal consumption expenditure.

In addition, the tax cut will increase the return on assets of the United States from the current 12% to 14.8%, which strengthens the US's advantage in return on investment, thereby enhancing the US siphon effect on global industrial capital. It is expected that the net inflow of industrial capital in the future will be Maintain at least $200 billion.

Huitong.com reminded that Trump will be the first to issue the draft tax law on Wednesday (November 1). Yujiro Goto, senior currency strategist at Nomura International in London, said that the US budget passed by Congress improved risk sentiment and boosted US Treasury yields.

According to Huitong.com, the US 10-year bond yield this week hit a new high of 2.4756, which also gave the US dollar index a certain upward momentum this week.

(US 10-year Treasury yield rate weekly chart)

(Dollar Chart Daily Chart)

From a technical point of view, the US dollar index has risen above the integer mark and the resistance around the 100-day moving average at 94.01 on the daily level. It also broke the resistance near the high of 94.27 on October 6th. The “head and shoulders†form was initially formed. It is expected to restart the mid-line rally. The resistance of the 61.8 retracement since 103.82 is around 98.94; the short-term initial resistance is at 95.16; 95.47 and 95.83, which are the July 20 high, the June 30 low and the July 14 respectively. The high point, while the 38.2% retracement resistance of the decline since 103 is also around 95.925.

Need to be reminded that the short-term US dollar index will continue to step back on the "head and shoulders" neckline near the support of 94.27 support needs to be vigilant.

In addition, the latest news on Friday (October 27) shows that Trump tends to favor the dovish Powell to be elected as the next Fed chairman, which has dragged down the gains of the US dollar and US debt.

Fourth, the next presidential candidate of the Fed will drive the market nerve, and the price of gold is still at risk.

Another focus of the financial market this week is the expected change in the Fed’s next presidential candidate, as this will determine the main tone of the Fed’s monetary policy in the coming years, and thus has received widespread attention in the financial market. Stanford University economist Taylor and the dovish Fed governor Powell still have the opportunity,

According to the latest reports from foreign media, the other three popular candidates, such as Yellen, have basically announced their exit. US President Trump tends to nominate the Fed’s Fed governor Powell to lead the Fed, which will mark the world’s largest economy’s monetary policy. Continuity.

According to the latest data from the US political forecast website PredictIt, among the top five Fed presidents in Trump, the current political bet on Powell's nomination for the next Fed chairman is the highest, exceeding 80%, reaching 84%.

The second-ranked economist Taylor’s chances of nominations fell sharply, less than one-eighth of Powell’s. Yellen’s chances of re-election are equal to that of Taylor, only 10%, and the former Fed governor Walsh, who is regarded as a hawkish figure by the market, has a chance of only 3%.

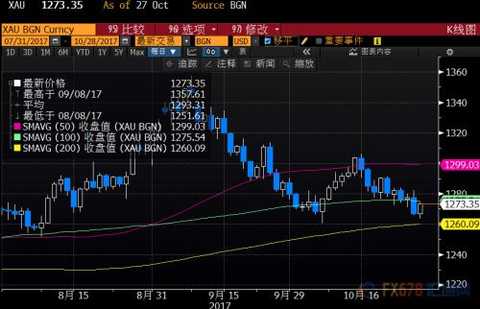

It is worth mentioning that last week, Taylor was the most likely to be elected as the next Fed chairman. This has provided support to the US dollar in the first half of this week, while the price of gold continues to be under pressure. It once refreshed the three-week low to $1,263.00 per ounce.

However, after Powell’s expectation that the next Fed chairman’s expectations will heat up, the US dollar index also fell from around the three-month high of 95.15 hit on Friday to around 94.81, while the situation in Spain was slightly pushed up to avoid the risk. The 200-day moving average support, closing up nearly 7 US dollars, closed at 1,273.35 US dollars / ounce, but still under pressure on the 100-day moving average, the downside risk has not been completely eliminated, the market bearish gold expectations have not been significantly improved.

According to a recent survey released by Bloomberg on Friday (October 27), gold traders and analysts are biased towards bearish gold movements next week. Of the 19 gold traders and analysts surveyed, 5 are bullish (26%) ), 8 people are bearish (42%) and 6 are flat (32%).

Need to be reminded that foreign media reported on Friday that the Catalonia local council with 70 votes, 10 votes against, 2 abstentions to declare the region independent from Spain; pushed up some risk aversion, investors next week It is also necessary to pay attention to the further development of the situation in Spain.

At present, Spanish Prime Minister Rajoy has stated that Spain does not accept independence in the region; the US State Department, the Office of the Prime Minister of the United Kingdom, the French President Mark Long, the German government and the Ukrainian government have all declared that they do not recognize the independence of Catalonia, and the President of the European Council, Tusk Said that the EU will only continue the Spanish government dialogue in the future. Analysts say that this risk aversion has limited support for gold prices.

Forex.com analyst Fawad Razaqzada believes that the price of gold is being promoted by Catalonia to promote independence, but this will not last long, because the dollar is still strong.

(Spot gold daily chart)

5. OPEC and other major oil producing countries may extend the period of production cuts, and oil prices will rise by 4% this week.

The crude oil market was supported by Saudi Arabia and Russia's comments on the extension of the production cut-off period. This week, international oil prices have withstood the negative impact of a sharp rebound in US production and an unexpected increase in crude oil inventories. The weekly line has risen by more than 4%, once more than seven months. The new high is $54.20/barrel.

The Organization of Petroleum Exporting Countries (OPEC) Secretary General Balkin said on Friday that before the next policy meeting of OPEC, Saudi Arabia and Russia announced their support for an extension of the oil production reduction agreement for another nine months. In addition, Saudi Crown Prince Salman said on Thursday that Saudi Arabia will support the extension of production cuts to stabilize oil demand and supply. And a few weeks ago, Russian President Vladimir Putin said that he supported the idea of ​​extending the production reduction agreement to 2018.

US investment bank Jefferies believes that if OPEC and its non-OPEC member states agree to extend the production reduction agreement for the entire 2018 year, then by 2019 the oil market will maintain a modest supply shortage.

According to a survey released by Bloomberg on Friday (October 27), crude oil traders and analysts turned to look at US crude oil prices next week.

(US crude oil main contract daily chart)

★ Next week, the financial market will welcome the "Super Week" storm

In the past week, the financial market has been very lively. Whether it is economic data or risk events, the market has experienced large fluctuations, but this week may be just an appetizer for the feast of the feast. Every day next week, there will be important economic data or heavy risk events that need to be focused on, and they may all trigger “stunning waves†in financial markets.

First, next Monday (October 30) will release the heavyweight US PCE price index and personal consumption expenditure data that the Fed will focus on.

In addition, next Tuesday (October 31) will usher in the Bank of Japan interest rate decision and the euro zone's third quarter GDP data.

Secondly, next Wednesday (November 1) will have more important US ISM manufacturing PMI data and Federal Reserve interest rate resolutions in September, while US President Trump will also announce the draft tax reform plan.

Then, next Thursday (November 2), the Bank of England will also announce interest rate resolutions, which may be the first rate hike in the UK in 10 years; the next Fed's next presidential candidate Powell and the permanent ballot Dudley will also replace the reference rate. Speech at the committee round table.

Finally, next Friday (November 3), there will still be a heavy US non-farm payroll report released.

It is worth reminding that White House officials have said that Trump will also announce the final candidate for the next Fed chairman before the trip to Asia on November 3.

Therefore, investors are also reminded here that it may be the most volatile market in the rest of the year, or it may be the biggest market in this year. It may be staged next week. It is necessary to take a good rest this weekend and adjust various aspects. Arrange the time and trading plan for the next week reasonably, which will help everyone to usher in a bumper week.

Traveling Supplies,disposable bed sheet set,nonwoven traveling supplies,compressed socks and towel

Sunshine Hygiene and Health Care Technology Jiangyin Co., Ltd , https://www.jyshygiene.com